Commercial Real Estate Loans are financial instruments developed to provide funding for different kinds of commercial residential or commercial property acquisitions, developments, and remodellings. These loans are normally secured by the residential or commercial property itself and are a crucial resource for businesses and investors looking to expand or enhance their real estate holdings. Different kinds of Commercial Real Estate Loans include:

Commercial Real Estate Loans are financial instruments developed to provide funding for different kinds of commercial residential or commercial property acquisitions, developments, and remodellings. These loans are normally secured by the residential or commercial property itself and are a crucial resource for businesses and investors looking to expand or enhance their real estate holdings. Different kinds of Commercial Real Estate Loans include:

1.Traditional Commercial Mortgages: These loans work likewise to domestic home loans, where the debtor receives a lump sum in advance and repays the loan quantity along with interest over a specified duration. They are commonly used for buying or re-financing homes such as office buildings, retail centers, and warehouses.

2.SBA 7( a) Loans: Offered by the Small Business Administration (SBA), these loans provide funding to small companies genuine estate acquisitions, construction, or refinancing. They frequently feature beneficial terms and lower deposit requirements.

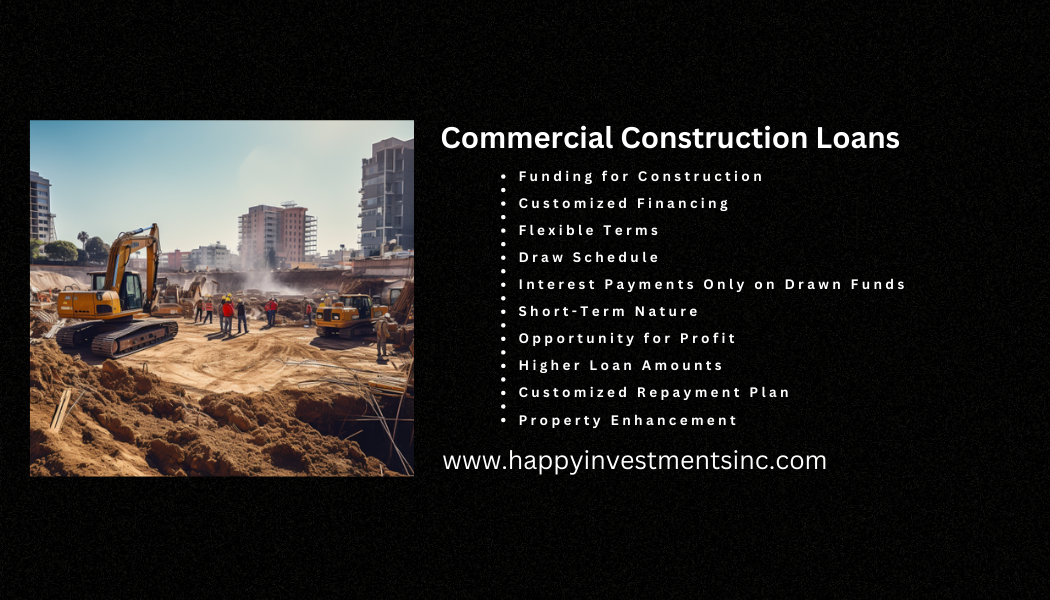

3.Commercial Construction Loans: These loans are designed to fund the building of brand-new commercial properties or significant restorations of existing ones. The funds are disbursed in phases as the building progresses.

4.Bridge Loans: Bridge loans supply short-term financing to bridge the space in between instant financing requirements and longer-term funding solutions. They are commonly used for time-sensitive transactions or when a home requires remodeling prior to it can qualify for irreversible funding.

5.Commercial Equity Loans: Also called equity lines of credit, these loans permit homeowner to use their home’s equity to money various company requirements, such as expansion, working capital, or enhancements.

6.CMBS Loans (Commercial Mortgage-Backed Securities): These loans include packaging a swimming pool of industrial realty loans into securities that are offered to investors. The earnings created from the hidden loans acts as security for the securities.

7.Hard Money Loans: These are short-term, high-interest loans frequently utilized by investor for fast acquisitions or to capitalize on time-sensitive chances.

8.Mezzanine Loans: Mezzanine financing sits in between senior debt and equity in a capital stack. It’s a way to protect additional funds using the property as collateral, frequently used for advancement jobs.

9.HUD/FHA Loans: Provided by the U.S. Department of Housing and Urban Development (HUD), these loans offer funding for multifamily homes, health care facilities, and other kinds of business real estate jobs.

10.Owner-Occupied Commercial Real Estate Loans: These loans are customized for companies that mean to occupy most of the residential or commercial property they buy. They frequently come with beneficial terms and lower deposit requirements.

Each kind of Commercial Real Estate Loan serves different functions and comes with varying terms, rates of interest, and eligibility requirements, permitting organizations and investors to select the financing choice that finest lines up with their requirements and objectives.

Commercial Hard Money loans are a kind of financing utilized in realty and service endeavors where conventional lending choices might be inaccessible due to the borrower’s credit rating or the unconventional nature of the job. These loans are usually protected by the worth of the property or possession, rather than the borrower’s credit reliability. Various kinds of Commercial Hard Money loans include:

Commercial Hard Money loans are a kind of financing utilized in realty and service endeavors where conventional lending choices might be inaccessible due to the borrower’s credit rating or the unconventional nature of the job. These loans are usually protected by the worth of the property or possession, rather than the borrower’s credit reliability. Various kinds of Commercial Hard Money loans include: A Commercial Bridge loan is a type of short-term funding service created to bridge the gap in between immediate capital requirements and more permanent, long-term financing. It is commonly utilized by companies and real estate investors to seize time-sensitive chances, address immediate monetary commitments, or help with property acquisitions. Commercial Bridge loans use versatility and speed, allowing customers to secure funds quickly while they work on getting a more conventional and sustainable funding source. There are numerous kinds of Commercial Bridge loans tailored to different circumstances:

A Commercial Bridge loan is a type of short-term funding service created to bridge the gap in between immediate capital requirements and more permanent, long-term financing. It is commonly utilized by companies and real estate investors to seize time-sensitive chances, address immediate monetary commitments, or help with property acquisitions. Commercial Bridge loans use versatility and speed, allowing customers to secure funds quickly while they work on getting a more conventional and sustainable funding source. There are numerous kinds of Commercial Bridge loans tailored to different circumstances: Commercial Construction loans are monetary instruments developed to money the advancement and construction of numerous types of commercial properties, varying from office buildings and retail centers to hotels and industrial facilities. These loans supply the necessary capital to cover the costs associated with land acquisition, architectural preparation, building materials, labor, and other expenses sustained during the building and construction procedure. Various sort of Commercial Construction loans include:

Commercial Construction loans are monetary instruments developed to money the advancement and construction of numerous types of commercial properties, varying from office buildings and retail centers to hotels and industrial facilities. These loans supply the necessary capital to cover the costs associated with land acquisition, architectural preparation, building materials, labor, and other expenses sustained during the building and construction procedure. Various sort of Commercial Construction loans include: The Small Business Administration (SBA) loans are financial help programs offered by the United States federal government to support and promote the development of small companies. These loans are designed to provide economical funding options to business owners and small business owners who may have difficulty obtaining loans through standard channels due to different factors, such as minimal security or credit history. There are several types of SBA loans offered, each tailored to particular service requirements:

The Small Business Administration (SBA) loans are financial help programs offered by the United States federal government to support and promote the development of small companies. These loans are designed to provide economical funding options to business owners and small business owners who may have difficulty obtaining loans through standard channels due to different factors, such as minimal security or credit history. There are several types of SBA loans offered, each tailored to particular service requirements: Business loans are monetary arrangements where a loan provider offers funds to a service entity to support its operational needs, growth, or other strategic initiatives. These loans play an essential function in helping with growth and preserving capital for companies. There are a number of types of service loans tailored to different functions and customer profiles:

Business loans are monetary arrangements where a loan provider offers funds to a service entity to support its operational needs, growth, or other strategic initiatives. These loans play an essential function in helping with growth and preserving capital for companies. There are a number of types of service loans tailored to different functions and customer profiles: Business Mortgage Loans Summerfield NC is a mortgage secured by industrial realty, for example, an office complex, shopping center, making storage facility, or apartment or condo or condo complex. Commercial mortgage loans resemble basic mortgage; but instead of borrowing funds to buy house, you secure any land or property for organization reasons.

Business Mortgage Loans Summerfield NC is a mortgage secured by industrial realty, for example, an office complex, shopping center, making storage facility, or apartment or condo or condo complex. Commercial mortgage loans resemble basic mortgage; but instead of borrowing funds to buy house, you secure any land or property for organization reasons.