Commercial Real Estate Loans are monetary instruments created to supply financing for various types of business residential or commercial property acquisitions, advancements, and renovations. These loans are normally secured by the home itself and are an important resource for companies and investors seeking to broaden or boost their real estate holdings. Different types of Commercial Real Estate Loans include:

- Traditional Commercial Mortgages: These loans work likewise to residential home mortgages, where the borrower receives a lump sum upfront and repays the loan amount in addition to interest over a specified period. They are commonly utilized for acquiring or re-financing properties such as office buildings, retail centers, and warehouses.

- SBA 7( a) Loans: Offered by the Small Business Administration (SBA), these loans provide financing to small companies for genuine estate acquisitions, construction, or refinancing. They frequently include beneficial terms and lower deposit requirements.

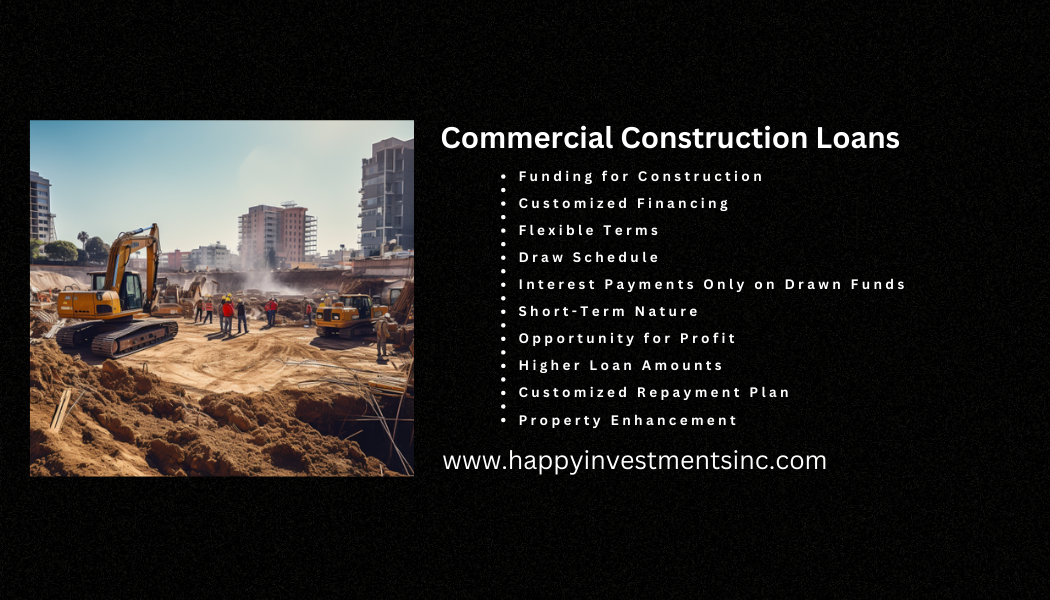

- Commercial Construction Loans: These loans are developed to money the building and construction of brand-new commercial homes or major remodelings of existing ones. The funds are disbursed in phases as the building advances.

- Bridge Loans: Bridge loans provide short-term funding to bridge the gap in between instant financing needs and longer-term funding solutions. They are typically utilized for time-sensitive transactions or when a home requires restorations before it can qualify for long-term financing.

- Commercial Equity Loans: Also referred to as equity lines of credit, these loans allow property owners to tap into their property’s equity to fund various service needs, such as expansion, working capital, or enhancements.

- CMBS Loans (Commercial Mortgage-Backed Securities): These loans include packaging a pool of business property loans into securities that are sold to financiers. The earnings generated from the underlying loans acts as security for the securities.

- Hard Money Loans: These are short-term, high-interest loans often used by real estate investors for quick acquisitions or to take advantage of time-sensitive chances.

- Mezzanine Loans: Mezzanine funding sits between senior financial obligation and equity in a capital stack. It’s a way to protect extra funds using the home as security, often utilized for development tasks.

- HUD/FHA Loans: Provided by the U.S. Department of Housing and Urban Development (HUD), these loans offer financing for multifamily homes, health care centers, and other kinds of business property jobs.

- Owner-Occupied Commercial Real Estate Loans: These loans are tailored for businesses that plan to occupy the majority of the residential or commercial property they acquire. They typically come with beneficial terms and lower deposit requirements.

Each kind of Commercial Real Estate Loan serves different functions and comes with differing terms, rates of interest, and eligibility requirements, allowing services and financiers to select the financing choice that best aligns with their requirements and goals.

Commercial Hard Money loans are a type of financing used in real estate and company ventures where traditional lending choices might be unattainable due to the customer’s credit history or the non-traditional nature of the project. These loans are usually secured by the worth of the property or asset, instead of the debtor’s credit reliability. Numerous types of Commercial Hard Money loans include:

Commercial Hard Money loans are a type of financing used in real estate and company ventures where traditional lending choices might be unattainable due to the customer’s credit history or the non-traditional nature of the project. These loans are usually secured by the worth of the property or asset, instead of the debtor’s credit reliability. Numerous types of Commercial Hard Money loans include: Commercial Construction loans are financial instruments developed to money for the advancement and construction of different kinds of business residential or commercial properties, ranging from office complexes and retail centers to hotels and industrial centers. These loans supply the essential capital to cover the costs associated with land acquisition, architectural preparation, building and construction materials, labor, and other costs sustained during the building procedure. Various kinds of Commercial Construction loans consist of:

Commercial Construction loans are financial instruments developed to money for the advancement and construction of different kinds of business residential or commercial properties, ranging from office complexes and retail centers to hotels and industrial centers. These loans supply the essential capital to cover the costs associated with land acquisition, architectural preparation, building and construction materials, labor, and other costs sustained during the building procedure. Various kinds of Commercial Construction loans consist of:

The Small Business Administration (SBA) loans are monetary help programs used by the United States government to support and promote the growth of small businesses. These loans are developed to provide budget-friendly financing options to business owners and small company owners who might have problems getting loans through conventional channels due to different reasons, such as minimal security or credit rating. There are a number of types of SBA loans offered, each customized to specific business requirements:

The Small Business Administration (SBA) loans are monetary help programs used by the United States government to support and promote the growth of small businesses. These loans are developed to provide budget-friendly financing options to business owners and small company owners who might have problems getting loans through conventional channels due to different reasons, such as minimal security or credit rating. There are a number of types of SBA loans offered, each customized to specific business requirements:

There are numerous forms of industrial loans. However, some of the most common are long-term loans, swing loan, commercial construction loans, and channel loans. The structure of the loan primarily consists of the principal (amount being lent) rate of interest and term (length of time of the loan). Other elements such as the customer’s credit ranking, the business property being used as security, basic market conditions, and so on, develop the structure of an industrial mortgage. Business property does not ought to be made complex. There are Owner-occupied company loans and financial investment realty loans. Call Today: (951) 963-9399.

There are numerous forms of industrial loans. However, some of the most common are long-term loans, swing loan, commercial construction loans, and channel loans. The structure of the loan primarily consists of the principal (amount being lent) rate of interest and term (length of time of the loan). Other elements such as the customer’s credit ranking, the business property being used as security, basic market conditions, and so on, develop the structure of an industrial mortgage. Business property does not ought to be made complex. There are Owner-occupied company loans and financial investment realty loans. Call Today: (951) 963-9399.