Commercial Real Estate Loans are financial instruments developed to offer financing for various kinds of business residential or commercial property acquisitions, advancements, and remodellings. These loans are generally secured by the property itself and are a crucial resource for organizations and investors aiming to broaden or improve their real estate holdings. Different type of Commercial Real Estate Loans include:

1.Traditional Commercial Mortgages: These loans function similarly to property mortgages, where the borrower gets a lump sum upfront and repays the loan amount in addition to interest over a specific duration. They are typically utilized for acquiring or re-financing residential or commercial properties such as office complex, retail centers, and storage facilities.

2.SBA 7( a) Loans: Offered by the Small Business Administration (SBA), these loans supply funding to small businesses for real estate acquisitions, building, or refinancing. They frequently include beneficial terms and lower deposit requirements.

3.Commercial Construction Loans: These loans are designed to fund the construction of brand-new commercial residential or commercial properties or major renovations of existing ones. The funds are paid out in stages as the building progresses.

4.Bridge Loans: Bridge loans provide short-term funding to bridge the space between instant funding needs and longer-term funding options. They are typically used for time-sensitive deals or when a property requires remodellings before it can receive permanent financing.

5.Commercial Equity Loans: Also referred to as equity lines of credit, these loans permit property owners to take advantage of their property’s equity to fund numerous service needs, such as expansion, working capital, or improvements.

6.CMBS Loans (Commercial Mortgage-Backed Securities): These loans include product packaging a pool of commercial property loans into securities that are offered to financiers. The earnings generated from the underlying loans functions as security for the securities.

7.Hard Money Loans: These are short-term, high-interest loans frequently used by investor for fast acquisitions or to profit from time-sensitive opportunities.

8.Mezzanine Loans: Mezzanine funding sits in between senior financial obligation and equity in a capital stack. It’s a method to secure additional funds utilizing the residential or commercial property as collateral, frequently utilized for advancement projects.

9.HUD/FHA Loans: Provided by the U.S. Department of Housing and Urban Development (HUD), these loans use funding for multifamily properties, healthcare facilities, and other kinds of commercial property tasks.

10.Owner-Occupied Commercial Real Estate Loans: These loans are tailored for services that plan to occupy the majority of the home they purchase. They often include favorable terms and lower down payment requirements.

Each type of Commercial Real Estate Loan serves various purposes and comes with varying terms, interest rates, and eligibility requirements, enabling organizations and financiers to pick the funding alternative that finest lines up with their requirements and objectives.

Commercial Hard Money loans are a kind of financing utilized in real estate and company ventures where traditional loaning choices might be unattainable due to the customer’s credit rating or the non-traditional nature of the project. These loans are generally secured by the worth of the home or property, instead of the debtor’s creditworthiness. Various kinds of Commercial Hard Money loans consist of:

Commercial Hard Money loans are a kind of financing utilized in real estate and company ventures where traditional loaning choices might be unattainable due to the customer’s credit rating or the non-traditional nature of the project. These loans are generally secured by the worth of the home or property, instead of the debtor’s creditworthiness. Various kinds of Commercial Hard Money loans consist of: A Commercial Bridge loan is a type of short-term funding service created to bridge the gap between immediate capital requirements and more permanent, long-lasting financing. It is frequently used by companies and real estate investors to take time-sensitive opportunities, address urgent financial commitments, or assist in residential or commercial property acquisitions. Commercial Bridge loans provide versatility and speed, enabling borrowers to secure funds quickly while they work on acquiring a more traditional and sustainable financing source. There are a number of type of Commercial Bridge loans tailored to various scenarios:

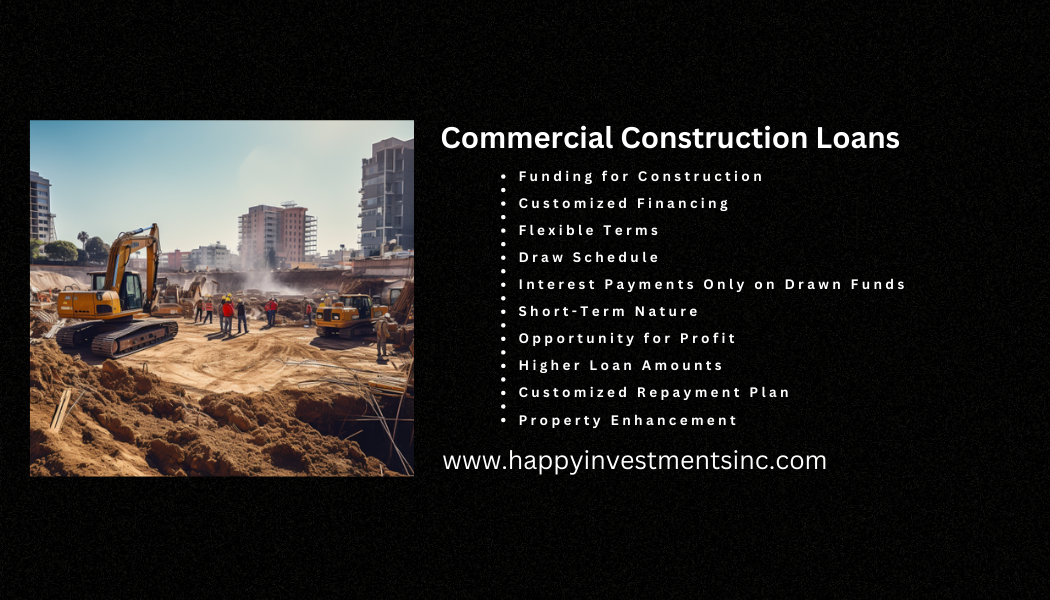

A Commercial Bridge loan is a type of short-term funding service created to bridge the gap between immediate capital requirements and more permanent, long-lasting financing. It is frequently used by companies and real estate investors to take time-sensitive opportunities, address urgent financial commitments, or assist in residential or commercial property acquisitions. Commercial Bridge loans provide versatility and speed, enabling borrowers to secure funds quickly while they work on acquiring a more traditional and sustainable financing source. There are a number of type of Commercial Bridge loans tailored to various scenarios: Commercial Construction loans are monetary instruments designed to fund the development and construction of numerous types of commercial properties, varying from office buildings and retail centers to hotels and commercial facilities. These loans offer the needed capital to cover the costs related to land acquisition, architectural preparation, building products, labor, and other expenditures sustained during the building and construction procedure. Different type of Commercial Construction loans include:

Commercial Construction loans are monetary instruments designed to fund the development and construction of numerous types of commercial properties, varying from office buildings and retail centers to hotels and commercial facilities. These loans offer the needed capital to cover the costs related to land acquisition, architectural preparation, building products, labor, and other expenditures sustained during the building and construction procedure. Different type of Commercial Construction loans include: The Small Business Administration (SBA) loans are financial help programs offered by the United States government to support and promote the development of small businesses. These loans are designed to supply cost effective funding alternatives to business owners and small company owners who might have trouble obtaining loans through conventional channels due to numerous factors, such as minimal security or credit history. There are a number of types of SBA loans readily available, each customized to particular company needs:

The Small Business Administration (SBA) loans are financial help programs offered by the United States government to support and promote the development of small businesses. These loans are designed to supply cost effective funding alternatives to business owners and small company owners who might have trouble obtaining loans through conventional channels due to numerous factors, such as minimal security or credit history. There are a number of types of SBA loans readily available, each customized to particular company needs: Business loans are monetary arrangements where a lending institution offers funds to a business entity to support its operational requirements, expansion, or other tactical initiatives. These loans play an essential function in facilitating growth and preserving cash flow for organizations. There are several types of business loans customized to numerous functions and customer profiles:

Business loans are monetary arrangements where a lending institution offers funds to a business entity to support its operational requirements, expansion, or other tactical initiatives. These loans play an essential function in facilitating growth and preserving cash flow for organizations. There are several types of business loans customized to numerous functions and customer profiles: Industrial Mortgage Loans North Carolina is a mortgage protected by industrial realty, for instance, a workplace complex, shopping plaza, manufacturing warehouse, or home or condominium complex. Business mortgage loans resemble basic mortgage; however instead of obtaining funds to buy house, you secure any land or property for business factors.

Industrial Mortgage Loans North Carolina is a mortgage protected by industrial realty, for instance, a workplace complex, shopping plaza, manufacturing warehouse, or home or condominium complex. Business mortgage loans resemble basic mortgage; however instead of obtaining funds to buy house, you secure any land or property for business factors.