Commercial Real Estate Loans are financial instruments developed to supply financing for different types of industrial property acquisitions, advancements, and renovations. These loans are typically secured by the property itself and are a vital resource for businesses and investors aiming to broaden or boost their realty holdings. Various sort of Commercial Real Estate Loans consist of:

1.Traditional Commercial Mortgages: These loans function likewise to property home mortgages, where the customer receives a lump sum upfront and pays back the loan quantity along with interest over a specific duration. They are commonly utilized for buying or refinancing properties such as office complex, retail centers, and storage facilities.

2.SBA 7( a) Loans: Offered by the Small Business Administration (SBA), these loans provide funding to small companies for real estate acquisitions, building, or refinancing. They typically feature beneficial terms and lower deposit requirements.

3.Commercial Construction Loans: These loans are developed to money the construction of new business homes or major remodeling of existing ones. The funds are paid out in stages as the building and construction advances.

4.Bridge Loans: Bridge loans supply short-term financing to bridge the space between immediate financing requirements and longer-term financing services. They are typically used for time-sensitive deals or when a property requires renovations before it can get approved for long-term funding.

5.Commercial Equity Loans: Also referred to as equity credit lines, these loans enable property owners to use their home’s equity to fund various company needs, such as expansion, working capital, or improvements.

6.CMBS Loans (Commercial Mortgage-Backed Securities): These loans involve packaging a pool of commercial property loans into securities that are sold to financiers. The income produced from the underlying loans functions as collateral for the securities.

7.Hard Money Loans: These are short-term, high-interest loans often used by investor for quick acquisitions or to capitalize on time-sensitive chances.

8.Mezzanine Loans: Mezzanine funding sits in between senior financial obligation and equity in a capital stack. It’s a method to secure extra funds utilizing the property as security, often used for development projects.

9.HUD/FHA Loans: Provided by the U.S. Department of Housing and Urban Development (HUD), these loans use funding for multifamily homes, healthcare centers, and other kinds of commercial property jobs.

10.Owner-Occupied Commercial Real Estate Loans: These loans are tailored for services that intend to inhabit most of the residential or commercial property they acquire. They typically come with beneficial terms and lower down payment requirements.

Each kind of Commercial Real Estate Loan serves different functions and comes with differing terms, rate of interest, and eligibility criteria, permitting companies and investors to choose the funding option that finest lines up with their needs and goals.

Commercial Hard Money loans are a kind of financing used in real estate and service endeavors where conventional lending alternatives might be unattainable due to the borrower’s credit history or the non-traditional nature of the project. These loans are generally protected by the worth of the property or asset, rather than the customer’s creditworthiness. Different type of Commercial Hard Money loans include:

Commercial Hard Money loans are a kind of financing used in real estate and service endeavors where conventional lending alternatives might be unattainable due to the borrower’s credit history or the non-traditional nature of the project. These loans are generally protected by the worth of the property or asset, rather than the customer’s creditworthiness. Different type of Commercial Hard Money loans include: A Commercial Bridge loan is a type of short-term funding option developed to bridge the gap between immediate capital requirements and more long-term, long-lasting funding. It is typically utilized by businesses and investor to seize time-sensitive opportunities, address immediate monetary obligations, or facilitate home acquisitions. Commercial Bridge loans offer flexibility and speed, enabling debtors to secure funds quickly while they work on getting a more conventional and sustainable funding source. There are several kinds of Commercial Bridge loans tailored to different circumstances:

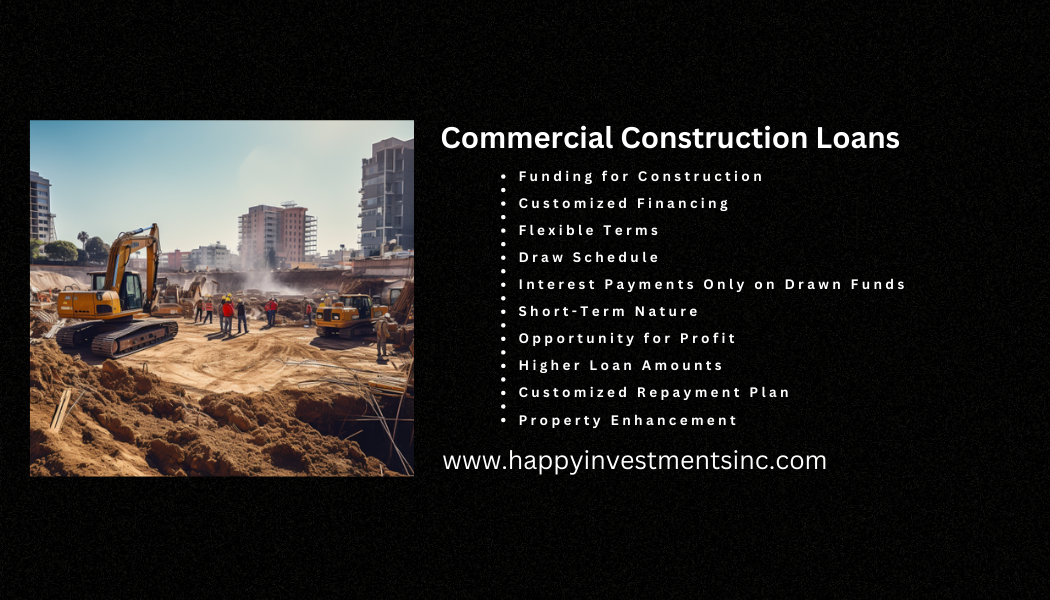

A Commercial Bridge loan is a type of short-term funding option developed to bridge the gap between immediate capital requirements and more long-term, long-lasting funding. It is typically utilized by businesses and investor to seize time-sensitive opportunities, address immediate monetary obligations, or facilitate home acquisitions. Commercial Bridge loans offer flexibility and speed, enabling debtors to secure funds quickly while they work on getting a more conventional and sustainable funding source. There are several kinds of Commercial Bridge loans tailored to different circumstances: Commercial Construction loans are monetary instruments created to fund the development and building of various types of industrial residential or commercial properties, ranging from office complex and retail centers to hotels and commercial centers. These loans provide the needed capital to cover the costs related to land acquisition, architectural planning, building products, labor, and other costs sustained during the construction process. Various sort of Commercial Construction loans consist of:

Commercial Construction loans are monetary instruments created to fund the development and building of various types of industrial residential or commercial properties, ranging from office complex and retail centers to hotels and commercial centers. These loans provide the needed capital to cover the costs related to land acquisition, architectural planning, building products, labor, and other costs sustained during the construction process. Various sort of Commercial Construction loans consist of: The Small Business Administration (SBA) loans are monetary help programs used by the United States government to support and promote the development of small companies. These loans are created to provide affordable financing options to business owners and small company owners who may have difficulty getting loans through conventional channels due to various factors, such as restricted security or credit rating. There are a number of types of SBA loans offered, each tailored to specific service needs:

The Small Business Administration (SBA) loans are monetary help programs used by the United States government to support and promote the development of small companies. These loans are created to provide affordable financing options to business owners and small company owners who may have difficulty getting loans through conventional channels due to various factors, such as restricted security or credit rating. There are a number of types of SBA loans offered, each tailored to specific service needs: Business loans are monetary arrangements where a lending institution offers funds to a service entity to support its operational needs, expansion, or other strategic efforts. These loans play a crucial function in facilitating development and keeping capital for organizations. There are a number of types of business loans tailored to various functions and debtor profiles:

Business loans are monetary arrangements where a lending institution offers funds to a service entity to support its operational needs, expansion, or other strategic efforts. These loans play a crucial function in facilitating development and keeping capital for organizations. There are a number of types of business loans tailored to various functions and debtor profiles: There are numerous types of commercial loans. Nevertheless, a few of the most typical are long-term loans, bridge loans, commercial construction loans, and channel loans. The structure of the loan mainly includes the principal (quantity being loaned) rate of interest and term (length of time of the loan). Other elements such as the debtor’s credit score, the business realty being applied as security, basic market conditions, and so on, establish the structure of a business home mortgage. Commercial home doesn’t should be made complex. There are Owner-occupied business loans and financial investment property loans. Call Today: (951) 963-9399.

There are numerous types of commercial loans. Nevertheless, a few of the most typical are long-term loans, bridge loans, commercial construction loans, and channel loans. The structure of the loan mainly includes the principal (quantity being loaned) rate of interest and term (length of time of the loan). Other elements such as the debtor’s credit score, the business realty being applied as security, basic market conditions, and so on, establish the structure of a business home mortgage. Commercial home doesn’t should be made complex. There are Owner-occupied business loans and financial investment property loans. Call Today: (951) 963-9399.